Borrowed Power: How Corruption Drives Tanzania’s Debt Crisis and Funds Samia’s Repression

Ujasusi Blog’s East Africa Monitoring Team | 02 April 2026 | 0250 BST

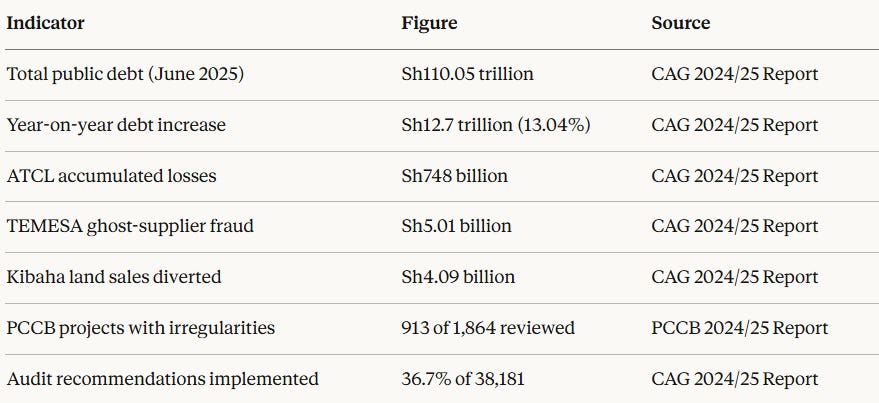

Tanzania’s CAG annual audit report presented to President Samia Suluhu Hassan on 30 March 2026 confirmed that total public debt had reached Sh110.05 trillion — a 13.04 per cent year-on-year rise — while state-owned enterprises accumulated hundreds of billions in losses and ghost-supplier fraud consumed key institutions. The audit documents a systemic financial governance failure that directly enables the Samia administration’s expanding repression: depleting the fiscal headroom needed to deliver public goods, intensifying popular grievances, and sustaining the security apparatus deployed to suppress them.

What Does the 2024/25 CAG Report Reveal About Tanzania’s Public Finances?

The 2024/25 audit covered 1,553 examinations — 1,339 financial statement audits, 18 performance audits, 12 real-time technical audits, 137 ICT system audits, and 147 special investigative audits — providing a comprehensive assessment of public financial management systems. The breadth of that operation reflects expanding institutional capacity. Capacity without enforcement yields documentation rather than accountability.

Air Tanzania Company Limited recorded losses of Sh191.19 billion in 2024/25 — a 108 per cent surge from the prior year — bringing national carrier accumulated losses to Sh748 billion since its revival. The Tanzania Railway Corporation suffered significant losses in 2024/25 partly attributed to 328 train accidents costing Sh3.06 billion in damages and lost revenue. In total, 22 state-owned commercial entities recorded losses over one or two consecutive years, reflecting deeper structural and operational challenges that remain unresolved. The pattern is not one of isolated mismanagement but of institutionalised financial haemorrhage across the parastatal sector.

What Does the Audit Reveal About Corruption Within State Institutions?

The 2024/25 report moves beyond aggregate loss figures to identify targeted fraud at the transactional level, and those findings carry greater analytical weight than parastatal performance data.

The Tanzania Electrical, Mechanical and Electronics Services Agency received the most severe assessment — an adverse audit opinion — with TEMESA ghost supplier fraud totalling Sh5.01 billion involving ghost suppliers and unverified services. Ghost-supplier fraud requires complicity from procurement officers, financial controllers, and in many cases senior management. Its presence at an agency responsible for critical government infrastructure indicates that internal control systems are either absent or deliberately circumvented.

Kibaha Town Council sold 168 plots worth Sh4.09 billion outside official systems, with funds diverted to private accounts. This is not administrative error. Selling public land through unofficial channels and routing proceeds to private accounts constitutes coordinated asset stripping of state property.

Tanzania’s tax collection authority holds Sh7.24 billion in uncollected tax debt outstanding for more than 17 years, while the Maritime Authority carries Sh658 million owed by the Mafia Island community unpaid for over 15 years. Debts of that age, at that scale, involving named institutions, point to deliberate non-enforcement — protection extended to debtors with sufficient political proximity to avoid consequences.

Of 38,181 recommendations issued in previous years, only 36.7 per cent had been fully implemented, meaning nearly two-thirds of identified problems across the public sector remain unaddressed despite formal audit instruction. That implementation gap is itself a governance indicator: CAG findings are received, acknowledged, and filed rather than acted upon.

What Does the PCCB Report Confirm About Systemic Corruption?

Tanzania’s anti-corruption bureau findings submitted alongside the CAG’s report on the same date reinforces rather than contradicts the audit’s conclusions.

The PCCB reviewed 1,864 projects and identified irregularities in 913 — nearly half — of which only 66 have been subjected to formal investigation, with monitored projects valued at Sh14.3 trillion, up from Sh11.4 trillion in 2023/24. The conversion rate from identified irregularity to formal investigation — 66 from 913, or 7.2 per cent — is the figure that demands analytical attention. For every ten projects flagged as problematic, nine face no formal investigation. Recurring deficiencies include weak contract management, payments for unexecuted work, non-compliance with procurement laws, and overpayments beyond contractual terms.

The PCCB simultaneously disclosed a Sh147.5 billion bank card fraud scheme — one of the largest financial crime busts in Tanzania’s recorded history — while reporting completion of investigations into 1,030 cases in 2024/25, up from 728 cases in 2023/24. The simultaneous presentation of expanded anti-corruption statistics alongside worsening audit findings is not a contradiction. It confirms that the PCCB operates as a selective enforcement instrument: active enough to generate credible-looking metrics, constrained enough to avoid pursuing the political networks that sustain high-level corruption. Independent governance monitoring of Tanzania consistently finds the bureau focused on low-level infractions, doing little to address graft committed by senior officials. That assessment aligns with the observable pattern: Sh147.5 billion in bank card fraud is investigated; the political economy enabling ghost-supplier networks at TEMESA and land-stripping at Kibaha is not.